Quick Answer

Usually no. Standard homeowners insurance policies in Texas exclude foundation damage caused by soil movement, settling, and expansive clay — and those causes are behind the large majority of foundation problems across Dallas-Fort Worth. Insurance may pay when the damage is the result of a sudden, accidental “covered peril,” most commonly a burst or leaking plumbing pipe under the slab. The deciding factor is always the cause of the damage — and your ability to document it.

TL;DR — Insurance & Foundation Repair

- Standard policies exclude foundation damage from “earth movement,” settling, and expansive soil.

- Most DFW damage is not covered because North Texas clay shrink-swell is the usual cause.

- Covered perils that can qualify: sudden plumbing leaks, burst pipes, fire, explosion, vehicle impact.

- Flooding and earthquakes are never covered by a standard policy — they need separate coverage.

- A plumbing leak under the slab is the most common path to an approved claim.

- Documentation wins claims: a dated plumbing test and an engineer’s report are critical.

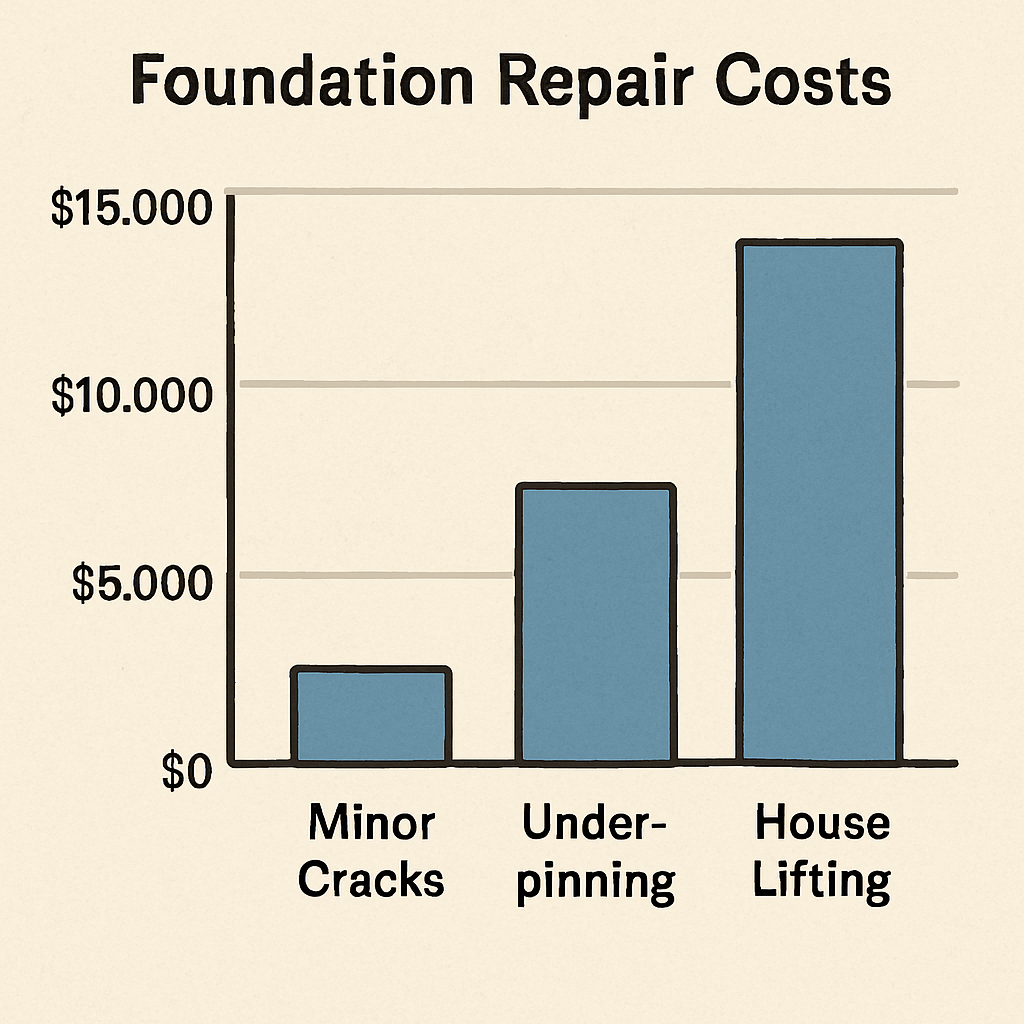

- If your claim is denied, 0% financing makes repair affordable — typical DFW repairs run $2,500–$15,000.

Does Homeowners Insurance Cover Foundation Repair?

It depends entirely on what caused the damage. A standard Texas homeowners policy (the HO-3 form most DFW homeowners carry) covers sudden and accidental losses from named perils. It specifically excludes gradual problems — and “earth movement,” soil settling, and expansive-clay shrink-swell are written into nearly every policy as exclusions.

That matters in North Texas more than almost anywhere else in the country. The Blackland Prairie clay under McKinney, Plano, Frisco, Allen, Dallas, Garland, and Fort Worth swells when it’s wet and shrinks when it’s dry. That seasonal movement — not a one-time accident — is what drives most foundation repair in the metro. Because it’s gradual and soil-related, it falls squarely inside the exclusion. You can read more about the mechanism on our causes of foundation problems page.

So the honest answer most DFW homeowners get is: your foundation movement itself is probably not covered — but if a covered event caused it, the picture changes.

What’s Covered vs. What’s Not

Here’s the simplest way to think about it. Insurance follows the cause, not the symptom. A cracked slab is not automatically covered or excluded — it depends on what cracked it.

| Cause of foundation damage | Typically covered? |

|---|---|

| Sudden burst or leaking plumbing pipe under the slab | Often yes — if sudden & accidental |

| Fire or explosion | Yes |

| Vehicle crashing into the home | Yes |

| Falling tree or heavy object | Sometimes |

| Expansive clay soil swelling and shrinking | No — earth-movement exclusion |

| Settling, cracking, or shrinkage over time | No |

| Drought drying and shrinking the soil | No |

| Poor original construction or grading | No |

| Tree-root pressure or moisture loss | No |

| Flooding or surface water | No — needs separate flood insurance |

| Earthquake / ground shifting from a quake | No — needs an earthquake endorsement |

| Lack of maintenance or poor drainage | No |

According to the Insurance Information Institute, earth movement and gradual settling are standard exclusions on home policies nationwide. Texas is no exception.

When Insurance Does Cover Foundation Repair

The most common approved claim in DFW starts under your slab. If a supply line or sewer pipe suddenly fails and washes out or saturates the soil beneath the foundation, the resulting movement can be tied to a covered water-damage event rather than to ordinary settling.

A few realities to understand before you count on it:

- The leak must be sudden and accidental, not a slow drip that’s been weeping for years. Insurers distinguish hard between the two.

- Coverage often pays to access and repair the leak (tear-out and plumbing) more readily than it pays to re-level the foundation itself. Policy language varies — read yours.

- Proof is everything. A dated hydrostatic plumbing test showing the failed line is the single most valuable piece of evidence you can have.

This is one reason every Stratum repair includes a pre-test and post-test plumbing check. Catching a leak isn’t just good engineering — it can be the difference between a denied claim and a covered one. The Texas Department of Insurance covers what standard policies include and exclude in its homeowners coverage guide.

Why Most DFW Foundation Claims Get Denied

If you’ve already been turned down, you’re in the majority — and it usually comes down to one of these:

1. The cause was soil movement

North Texas sits on some of the most expansive clay in the U.S., per the Texas Water Development Board. When the adjuster’s report names “soil movement,” “settling,” or “expansive soil,” the earth-movement exclusion applies and the claim is denied.

2. The damage was gradual

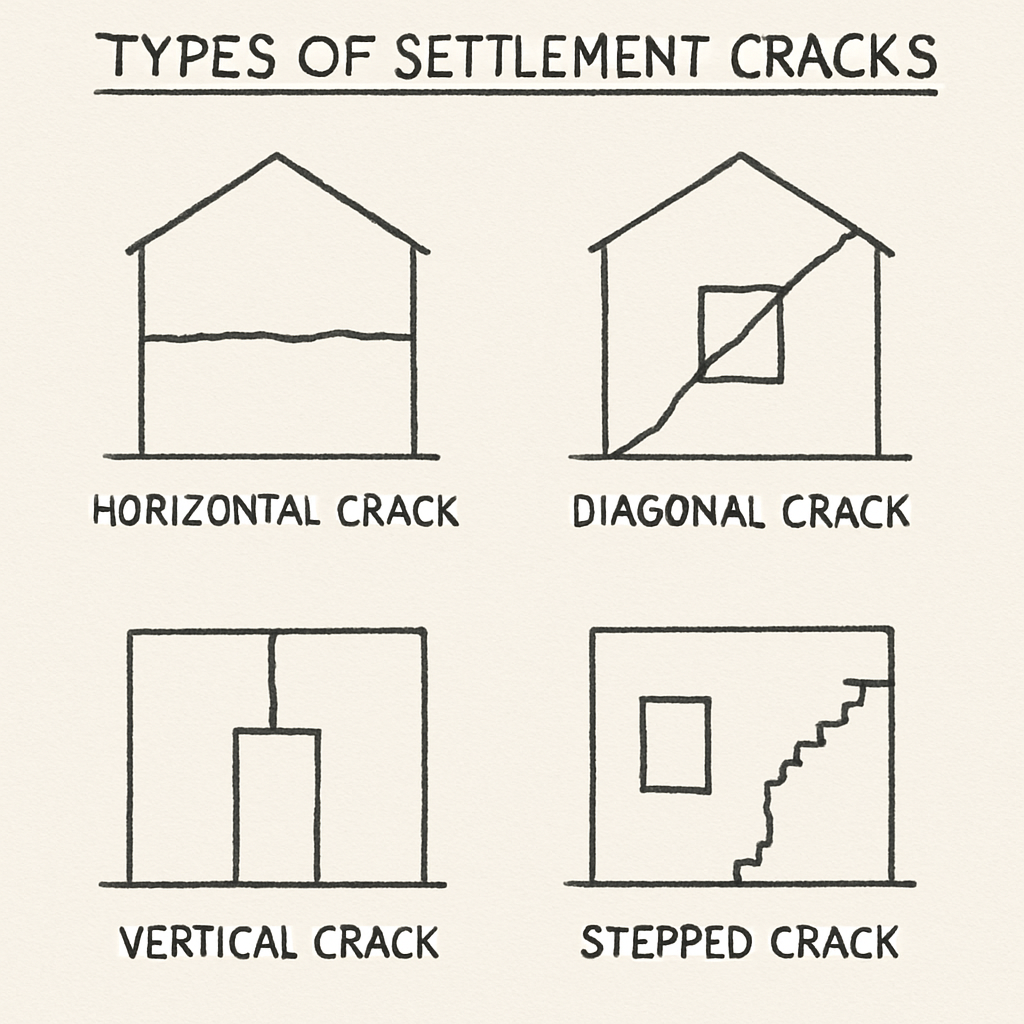

Hairline cracks that widened over several seasons read as wear-and-tear, not a sudden loss. Policies are built to cover accidents, not slow deterioration.

3. There was no covered peril behind it

No burst pipe, no fire, no vehicle — just a sticking door and a stair-step crack in the brick. Without a triggering event, there’s nothing for the policy to attach to.

4. A maintenance or drainage issue contributed

Poor grading, downspouts dumping at the slab, or an unwatered foundation during a Texas drought are considered preventable. Insurers treat them as homeowner responsibility.

Can You Add Foundation Coverage to Your Policy?

Sometimes. A handful of Texas carriers offer optional endorsements that broaden water-damage or slab-leak coverage. These add-ons won’t cover ordinary clay movement, but they can improve your position when a plumbing failure is involved. Ask your agent specifically about:

- Extended or “expanded” water damage endorsements

- Slab leak / under-slab plumbing coverage

- Service line coverage for buried pipes

Read the exclusions page of any quote before you assume foundation work is included. The base policy almost never is.

How to Give Your Claim the Best Chance

If you believe a covered peril caused your foundation problem, the process you follow matters as much as the facts.

- Document early. Photograph cracks, sticking doors, and any water before anything is touched.

- Get a plumbing test. A dated hydrostatic test that identifies a failed line is your strongest evidence.

- Get an engineer’s report. A stamped letter that links the damage to the covered event carries real weight with adjusters.

- File promptly. Delays let insurers argue the loss was gradual.

- Keep every record. Save the inspection report, photos, and all written communication.

A free Stratum inspection gives you the marked diagram and documentation you’ll need either way — whether you end up filing a claim or paying out of pocket. See how the visit works on our free foundation inspection page.

What If Insurance Won’t Pay?

For most DFW homeowners, foundation repair ends up being an out-of-pocket investment — and the good news is it’s more affordable than a denied claim makes it feel. Typical repairs in the metro run $2,500 to $15,000 depending on the number of piers and the pier system. You can see the full breakdown in our 2026 DFW pricing guide.

Stratum offers 0% interest financing with no payments for 6, 12, or 24 months through Momnt, so you can stabilize the home now and spread the cost out. We walk through every option — including home equity, pay-at-closing for sellers, and lender programs — in our companion guide, how to pay for foundation repair, and on our financing page.

Key Takeaways

- Standard Texas homeowners insurance excludes foundation damage from soil movement and settling.

- Coverage hinges on the cause — a sudden plumbing leak or other covered peril can qualify.

- Most DFW claims are denied because expansive clay is the underlying cause.

- Flood and earthquake damage require separate coverage.

- A dated plumbing test and engineer’s report are your best evidence for a claim.

- If the claim is denied, 0% financing keeps a $2,500–$15,000 repair manageable.

Frequently Asked Questions

Does homeowners insurance cover foundation repair in Texas?

Usually not. Standard Texas homeowners policies exclude foundation damage caused by soil movement, settling, and expansive clay — the most common causes in DFW. Coverage is possible only when a sudden covered peril, such as a burst plumbing pipe under the slab, caused the damage.

What kind of foundation damage is covered by insurance?

Damage that results from a sudden, accidental covered peril — a burst or leaking pipe under the slab, fire, explosion, or a vehicle striking the home. Gradual cracking and settling from soil movement is excluded.

Why was my foundation insurance claim denied?

The most common reason is that the adjuster attributed the damage to soil movement, settling, or expansive clay, all of which are standard policy exclusions. Claims are also denied when the damage is judged gradual, when no covered peril triggered it, or when a maintenance or drainage issue contributed.

Does insurance cover foundation damage from a plumbing leak?

Often, yes — if the leak was sudden and accidental. A pipe that bursts under the slab and washes out the soil can be tied to a covered water-damage event. A slow leak that weeped for years is typically treated as wear-and-tear and excluded. A dated plumbing test is essential proof.

Does flood insurance cover foundation repair?

Standard homeowners insurance never covers flooding; that requires a separate flood policy through the National Flood Insurance Program or a private insurer. Even then, flood policies have specific rules about foundation elements, so review the terms carefully.

Will adding an endorsement cover my foundation?

Some Texas carriers offer extended water-damage or slab-leak endorsements that can help when a plumbing failure is involved. None cover ordinary expansive-clay movement. Ask your agent to show you the exclusions in writing before assuming foundation work is included.

How do I prove my foundation damage was caused by a covered peril?

Document everything early with photos, get a dated hydrostatic plumbing test to identify a failed line, and obtain a stamped engineer’s report linking the damage to the covered event. File promptly so the insurer can’t argue the loss was gradual.

How much does foundation repair cost if insurance won’t pay?

Most DFW foundation repairs run between $2,500 and $15,000, depending on the number of piers and the system used. Stratum offers 0% interest financing with no payments for 6, 12, or 24 months so you can spread out the cost.

Should I file a claim before or after a foundation inspection?

Get the inspection first. A free Stratum inspection gives you the marked pier diagram, photos, and documentation you’ll need to file a credible claim — and tells you whether a covered peril is even involved before you open a claim.

Does a foundation insurance claim raise my premium?

It can. Filing any claim may affect your rate or renewal, and a denied claim still appears in your loss history. Weigh the likely payout against the long-term premium impact, especially if a covered peril isn’t clearly involved.

Does insurance cover the cosmetic damage after foundation repair?

If the underlying foundation claim is covered, related cosmetic repair may be included; if the foundation cause is excluded, the cosmetic work is too. Either way, Stratum’s sister company Stratum Homeworks handles drywall, paint, and tile touch-up after the lift under one warranty.

Find Out What’s Actually Wrong — Free

Free inspection. Marked pier diagram. The documentation you need for a claim or a quote.

Call (214) 302-8559 to schedule by phone.

Sources & Methodology

This guide reflects how standard Texas homeowners policies treat foundation damage as of 2026, cross-referenced against the following authoritative sources:

- Insurance Information Institute (III) — standard policy perils and the earth-movement exclusion (iii.org)

- Texas Department of Insurance (TDI) — Texas-specific homeowners coverage, exclusions, and endorsements (tdi.texas.gov)

- Texas Water Development Board — expansive clay soil behavior across North Texas (twdb.texas.gov)

- Stratum claim-support experience — documentation that has supported approved plumbing-related claims across 5,000+ DFW jobs since 2006

This article is general information, not insurance or legal advice. Coverage depends on your specific policy, carrier, and the facts of your loss — always read your policy and consult your agent.

About Stratum Foundation Repair: Founded 2006. Headquartered at 1402 Custer Rd #904, McKinney, TX 75070. 4.9-star Google rating across 519 reviews from six DFW offices. Lifetime transferable warranty on all pier installations.

Recent Comments